Everywhere you look, there are peaks. Economic indicators, corporate earnings, commodity prices, even global monetary policy support—all appear to have reached a natural limit and have nowhere to go but down. A loss of momentum after “peak everything” will inevitably trouble investors already worried about the U.S. economy’s staying power and the prospect of higher inflation.

Yet a slowdown is likely to take us to a level that will still be well above the sluggish pace of the pre-pandemic years. Does that mean living with higher inflation? Yes. But it also means a stronger economy.

The extraordinary responses to the pandemic by the Federal Reserve and Congress helped blunt the economic blow of lockdowns and set the stage for a powerful recovery. The effects of those efforts aren’t going away anytime soon, and as chief equity strategist of Bloomberg Intelligence, I anticipate consumer demand staying strong for longer than many expect.

The sheer size of federal outlays since the onset of the pandemic is stunning—the spending included in the U.S. fiscal packages was equal to about a quarter of 2020 gross domestic product, resulting in the largest deficit in U.S. history. Theory has it that the primary risk of unconstrained government spending is inflation once the economy reaches full employment. With the unemployment rate already back to a level it took five years to reach following the financial crisis, and the Biden administration pushing for more spending, we’re about to test that theory.

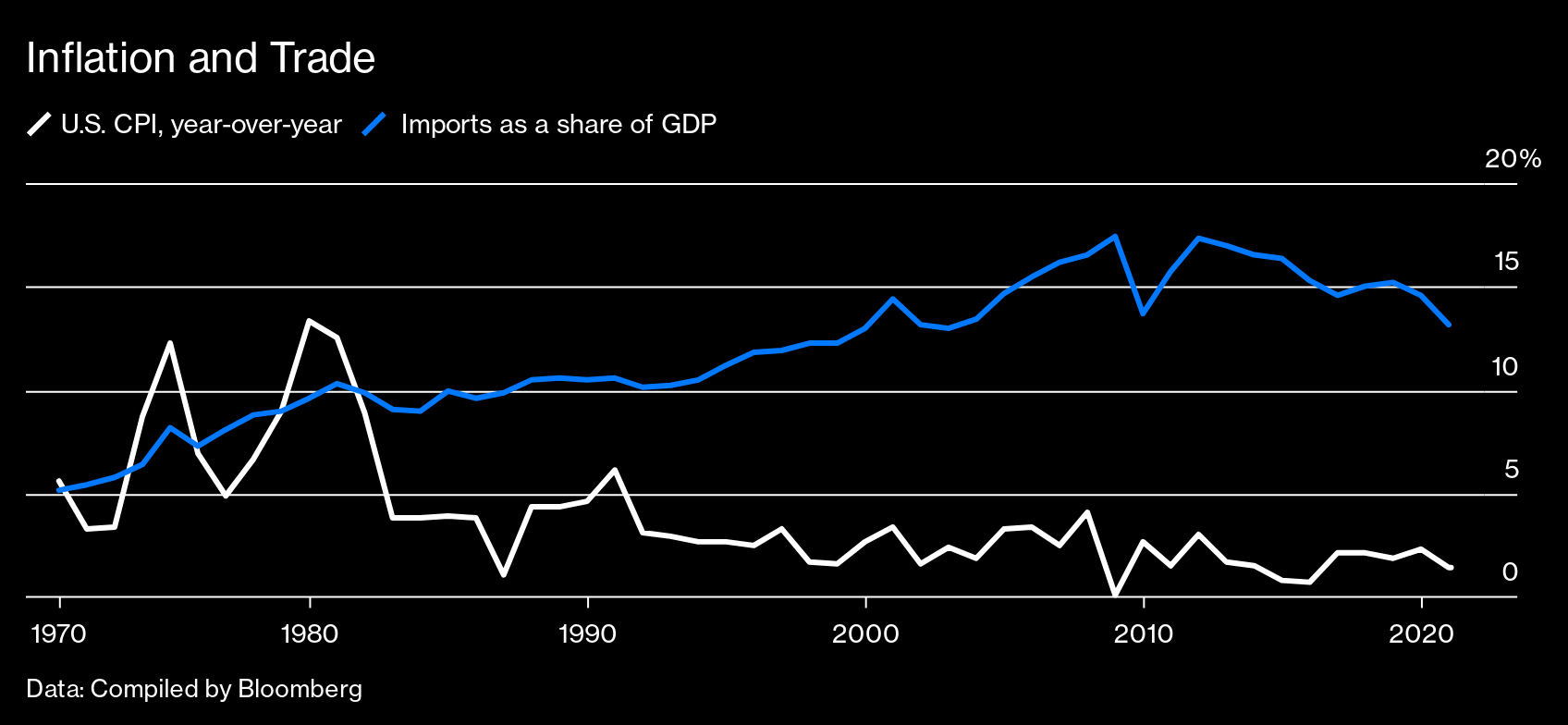

Inflation and Trade

Data: Compiled by Bloomberg

The Fed’s willingness to maintain its easy monetary policy, combined with a greater tolerance for inflation, has also supported growth, and adds to the case that inflation may settle in at a higher average level in the years ahead. The U.S. central bank is still following a crisis-era playbook—buying bonds and keeping interest rates low—and seems committed to staying the course. More evidence: Almost a year ago, the Fed signaled a change in inflation tolerance for the 2020s recovery. In an effort to pursue maximum employment that is broad-based and inclusive, the Fed adopted an average inflation target, communicating that it’s likely to allow inflation to exceed 2% and provide more accommodative monetary policy well into economic expansion, as a way to boost employment among workers in low- and moderate-income communities.

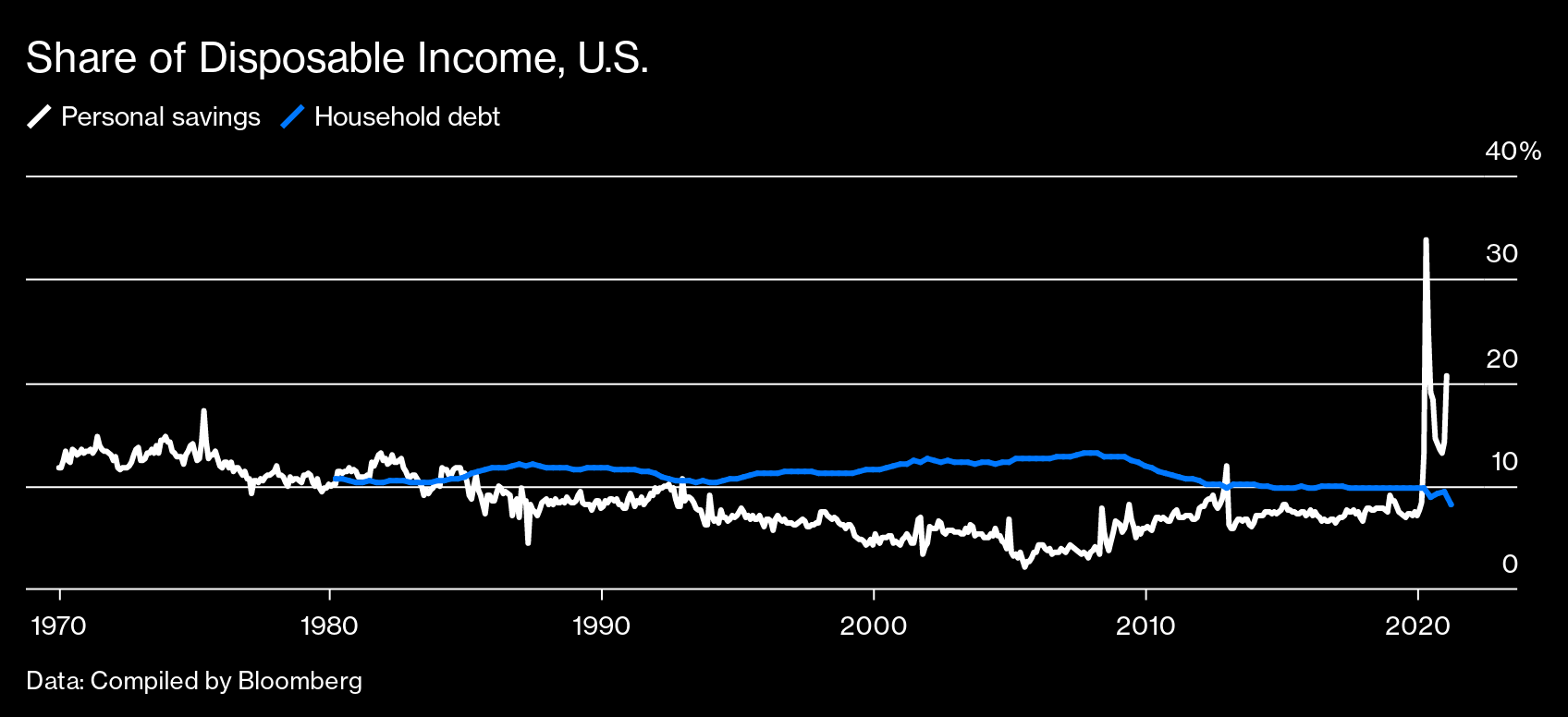

The result of the combined monetary and fiscal policy bonanza of 2020-21 is that household and company coffers are stuffed with cash waiting to be deployed. Corporate capital spending as a share of S&P 500 company sales is still near an all-time low, creating a coiled spring for the cycle ahead. Likewise, the ratio of personal savings to disposable income is near levels last recorded more than four decades ago. One reason for that is households’ debt service burden sits at a record low thanks to extremely low interest rates, which many consumers locked in as part of a giant mortgage refinancing rush.

Share of Disposable Income, U.S.

Data: Compiled by Bloomberg

Most current views of inflation suggest “transitory” price pressures brought on by pandemic-induced bottlenecks will ultimately fade. Economies will reopen and supplies of everything from workers to commodities will normalize, paving the path for lower inflation and a return to the 2010s. However, this thesis fails to acknowledge changes to the international trade landscape that occurred in recent years. Clearing some supply chain bottlenecks is indeed likely to ease inflation pressure in coming months. But corporations aren’t going to halt their efforts to shorten, diversify, and deglobalize supply chains as insurance against future shutdowns. The longer the pandemic extends, the more likely companies will respond.

Their top concern remains the supply chain, mentions of which shot up in conference calls during U.S. earnings season. “Supply chain” was mentioned 1,272 times in transcripts—matching records when tariff announcements first surprised financial markets in 2018, and suggesting a high amount of anxiety over product sourcing.

Technology, the center of the nationalistic rift between the U.S. and China, is a key part of supply chain concerns, and the sector’s innovation and use of low-cost global suppliers was a significant source of price deflation over the past two decades. That trend may now be under threat as policymakers erect further barriers to trade.

Higher costs are the natural result of both corporations’ effort to prevent future disruption and policymakers’ desire to gain control of their supply chains, and both will likely enlarge a wave of deglobalization that’s been taking shape for the better part of a decade. Indeed, it’s now looking like the multidecade era of trade expansion actually peaked in 2008 (which happened to coincide with inflation’s record low in the U.S.). If expansion of global trade is increasingly hobbled, higher inflation seems likely.

Even so, the U.S. is in no way headed back to the Great Inflation of the 1970s. Wages no longer rise rapidly in response to lower unemployment as they did then, when unions were stronger, economies less interconnected, and automation not as much of a force. Today’s policymakers also have the ’70s experience to draw upon and are less likely to repeat their predecessors’ mistakes.

Growth is also extremely unlikely to revert back to the disappointingly slow pace of the 2010s, given vast changes in the economic and policy landscape in recent years. Hints of a new paradigm were emerging leading into the pandemic, and the crisis response ensured that the 2020s will write a new growth and inflation story.

In other words, and quite contrary to current popular sentiment, there are good reasons to be optimistic about the economic outlook.

"peak" - Google News

July 30, 2021 at 11:01AM

https://ift.tt/3rFYCoN

What Comes After Peak Everything? A Not-So-Bad New Normal: Adams - Bloomberg

"peak" - Google News

https://ift.tt/2KZvTqs

https://ift.tt/2Ywz40B

Bagikan Berita Ini

0 Response to "What Comes After Peak Everything? A Not-So-Bad New Normal: Adams - Bloomberg"

Post a Comment